Case Studies

CASE STUDY 1 -

BACKGROUND

Pat and Deirdre live in Co. Mayo, and prior to 2010 ran a family business in a small rural town.

The family business was run by Pat as a sole trader. While Deirdre was not a registered owner of the business, she did personally guarantee many of the business debts.

The business encountered financial difficulties during 2008. Without the ability to restructure and refinance debts, Deirdre’s mother agreed for her home to be transferred to Pat and Deirdre so they could raise a mortgage loan to recapitalize their business. Unfortunately, despite the additional money introduced, the business ceased trading in 2010 leaving the debtors with debts of greater than €1.5M.

Prior to the business closing the couple’s modest family home worth just €105,000 was unencumbered. When Pat and Deirdre contacted their Personal Insolvency Practitioner (“PIP”) Mitchell O’Brien, the primary mortgage debt on the second property (Deirdre’s mother’s home) was €76,000. However, creditors moved quickly in attaining judgments, and registering same as judgment mortgages against both properties.

Once Pat filed the last of his outstanding tax returns, the Revenue Commissioners ‘opted-in’ to his PIA when requested to by the PIP. Deirdre didn’t have any excludable debts, i.e. Revenue debt.

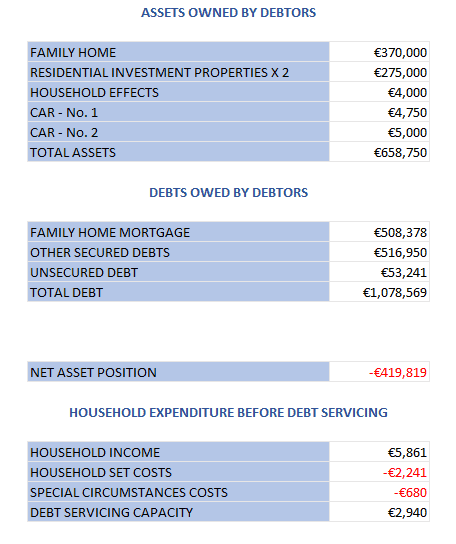

When the PIP secured Protective Certificates for these debtors, there were 6 secured debts totaling €383,478 secured against their two properties with a combined current market value of €220,000. The table below is a summary of the debtors’ Prescribed Financial Statements (“PFS”).

THE PIA SOLUTION CONSTRUCTED BY PIP AND APPROVED BY CREDITORS

Prior to the PIA process commencing, both Pat and Deirdre had secured employment. Pat is working full time as a PAYE’d employee; and Deirdre has a part-time PAYE’d job. Pat is supplied with a company vehicle as part of his employment.

The interlocking PIAs for Pat and Deirdre provide for the judgment mortgage (“JM”) that was the first charge on their family home being restructured as an annuity loan over 312 months to age 68, with a fixed interest rate of 2%, and a monthly payment of €432 (the 2% interest rate being the Court interest rate the creditor came into the PIA process with). The primary mortgage on the second property was restructured over 196 months at an interest rate of 3.65% (the relevant creditor’s standard variable rate), and a monthly payment of €518.

Pat and Deirdre retain both properties in their PIAs, and the two secured debt payments are included in the debtors’ Reasonable Living Expenses (“RLEs”) calculation. The mortgage payments relating to the second property have been included as a Special Circumstance Cost along with basic private health insurance due to a pre-existing health condition in the family.

Pat and Deirdre are now solvent, and will continue to remain solvent so long as they adhere to the terms of their Personal Insolvency Arrangements. Each of the judgment mortgages for which there was no equity at the commencement of the PIAs will be discharged by the creditors concerned on the successful completion of the Court approved arrangements by the debtors.

The table hereunder shows the debt Pat and Deirdre entered the Personal Insolvency process with, the payments made during the 6-year period of their PIAs, the amount of debt written off in the process, and the secured debt continuing after the process.

RATIONALE FOR CREDITORS’ SUPPORTING THE PIAS OF PAT AND DEIRDRE

The tables below detail the outcomes Pat and Deirdre’s creditors in both their PIAs, and separately in bankruptcy. Creditors acted rationally, and in their own best interests, in supporting these PIAs that were approved at recent creditors’ meetings.

CASE STUDY 1 -

BACKGROUND

Pat and Deirdre live in Co. Mayo, and prior to 2010 ran a family business in a small rural town.

The family business was run by Pat as a sole trader. While Deirdre was not a registered owner of the business, she did personally guarantee many of the business debts.

The business encountered financial difficulties during 2008. Without the ability to restructure and refinance debts, Deirdre’s mother agreed for her home to be transferred to Pat and Deirdre so they could raise a mortgage loan to recapitalize their business. Unfortunately, despite the additional money introduced, the business ceased trading in 2010 leaving the debtors with debts of greater than €1.5M.

Prior to the business closing the couple’s modest family home worth just €105,000 was unencumbered. When Pat and Deirdre contacted their Personal Insolvency Practitioner (“PIP”) Mitchell O’Brien, the primary mortgage debt on the second property (Deirdre’s mother’s home) was €76,000. However, creditors moved quickly in attaining judgments, and registering same as judgment mortgages against both properties.

Once Pat filed the last of his outstanding tax returns, the Revenue Commissioners ‘opted-in’ to his PIA when requested to by the PIP. Deirdre didn’t have any excludable debts, i.e. Revenue debt.

When the PIP secured Protective Certificates for these debtors, there were 6 secured debts totaling €383,478 secured against their two properties with a combined current market value of €220,000. The table below is a summary of the debtors’ Prescribed Financial Statements (“PFS”).

THE PIA SOLUTION CONSTRUCTED BY PIP AND APPROVED BY CREDITORS

Prior to the PIA process commencing, both Pat and Deirdre had secured employment. Pat is working full time as a PAYE’d employee; and Deirdre has a part-time PAYE’d job. Pat is supplied with a company vehicle as part of his employment.

The interlocking PIAs for Pat and Deirdre provide for the judgment mortgage (“JM”) that was the first charge on their family home being restructured as an annuity loan over 312 months to age 68, with a fixed interest rate of 2%, and a monthly payment of €432 (the 2% interest rate being the Court interest rate the creditor came into the PIA process with). The primary mortgage on the second property was restructured over 196 months at an interest rate of 3.65% (the relevant creditor’s standard variable rate), and a monthly payment of €518.

Pat and Deirdre retain both properties in their PIAs, and the two secured debt payments are included in the debtors’ Reasonable Living Expenses (“RLEs”) calculation. The mortgage payments relating to the second property have been included as a Special Circumstance Cost along with basic private health insurance due to a pre-existing health condition in the family.

Pat and Deirdre are now solvent, and will continue to remain solvent so long as they adhere to the terms of their Personal Insolvency Arrangements. Each of the judgment mortgages for which there was no equity at the commencement of the PIAs will be discharged by the creditors concerned on the successful completion of the Court approved arrangements by the debtors.

The table hereunder shows the debt Pat and Deirdre entered the Personal Insolvency process with, the payments made during the 6-year period of their PIAs, the amount of debt written off in the process, and the secured debt continuing after the process.

RATIONALE FOR CREDITORS’ SUPPORTING THE PIAS OF PAT AND DEIRDRE

The tables below detail the outcomes Pat and Deirdre’s creditors in both their PIAs, and separately in bankruptcy. Creditors acted rationally, and in their own best interests, in supporting these PIAs that were approved at recent creditors’ meetings.

CASE STUDY 2 -

BACKGROUND

Tim and Anne live in a modest 3 bed semi-detached home on the outskirts of a larger town in the South East.

Tim aged 59, had worked for the same company for 25 years until that business closed its Irish operation in 2010. Tim has completed a number of courses, but at his age, and where he lives, opportunities for future employment are not plentiful. Tim receives social welfare (job seeker’s allowance). Anne is aged 53 and works full time in a retail outlet. Anne’s job is permanent, and is thought to be secured to age 65.

This couple’s debts became unsustainable after Tim lost his job, and the redundancy payment received was spent meeting day to day living expenses over an extended period. Tim and Anne prioritized their family home mortgage payments as best they could, but fell into long term arrears. Their mortgage lender commenced the legal process of repossessing their home.

It was at this point that Tim and Anne contacted their local MABS office. MABS advised that this couple should meet with a Personal Insolvency Practitioner (“PIP”) and gave them a voucher to cover the cost.

Within two weeks of having met with the PIP Mitchell O’Brien based in Dungarvan, Co. Waterford, the PIP had secured Protective Certificates (“PCs”) that were issued by the South-Eastern Circuit Court on 20th March 2017. These PCs prevented any of Tim and Anne’s creditors from acting against them for a period of 70-days, during which time their creditors were forced to deal with the PIP (if the creditors don’t engage with the PIP during the PC period, the PIA can proceed without their input, and could well see their entire debt written-off with no payments to that creditor).

The table below is a summary of the debtors’ Prescribed Financial Statements (“PFS”) at the start of the PIA process:

THE PIA SOLUTION CONSTRUCTED BY THE PIP AND APPROVED BY CREDITORS

The PIP proposed interlocking PIAs for Tim and Anne that restructured the mortgage on their family home in the following ways:

- The interest rate was reduced from 4.3% and fixed at 0.5% for the 6-year period of the PIAs, reverting to 4.3% fixed for the remaining restructured mortgage term.

- The term was reduced from age 72 for Tim to age 65 for Anne (12-years).

- The mortgage balance owed was reduced by €30,000 immediately on the commencement of the PIAs.

- The mortgage will continue to reduce each month during the PIA

- Modest payments are to be made to creditors with unsecured debts that will be written off at the end of the term of the PIA.

- Tim and Anne retain their family home with a sustainable and performing mortgage loan.

Tim and Anne are now solvent, and will continue to remain solvent so long as they adhere to the terms of their Personal Insolvency Arrangements. All of their unsecured debts, and €30,000 of their mortgage will be written off in their PIA.

The table hereunder shows the debts Tim and Anne entered the Personal Insolvency process with, the payments made during the 6-years period of their PIAs, the amount of debt written off in the process, and the secured debt continuing after the process:

RATIONALE FOR CREDITORS’ SUPPORT OF PIAS FOR MR & MRS DEBTOR

The tables below detail the outcomes for Tim and Anne’s creditors in a PIA scenario and in Bankruptcy. Creditors acted rationally, and in their own best interests, in supporting these PIAs. The table below details the differing outcomes for creditors between the PIAs and the alternative of bankruptcy.

CASE STUDY 3 -

BACKGROUND

Brendan and Alice live in a rural location outside a small town in the South East of the Country. They have two sons in secondary school. Both children experience health difficulties for which there is on-going medical expenditure required. Brendan aged 45 is a public servant with a permanent employment contract. Alice is also employed full-time.

This couple’s debts became unsustainable after borrowing to build a detached family home in 2007 before selling their previous home. They borrowed from a sub-prime lender to build their new home at a high interest rate. The expectation was that they would refinance the sub-prime debt with a main stream mortgage lender when the new house was completed and the former home was sold. However, the new home was completed after the property crash and resulting recession of 2008. This couple also had a residential investment property.

Both incomes dropped in 2009/2010 as a result of increased taxes and a reduction in overtime. The rental incomes derived from the two rental properties was low during this period, and Brendan and Alice were unable to meet their financial commitments as and when they fell due.

Brendan and Alice consulted a number of debtor advocacy groups who suggested they should bankrupt themselves. They were advised the continued ownership of their home would be jeopardised in bankruptcy. Brendan and Alice contacted the Personal Insolvency Practitioner (“PIP”) Mitchell O’Brien who advised they should apply for a Personal Insolvency Arrangement (“PIA”) which would return them to solvency and seek to protect their family home.

Within four weeks of having met with the PIP, the PIP had secured Protective Certificates (“PCs”), issued by the South-Eastern Circuit Personal Insolvency Court on 5th September 2016. These PCs prevented any of Brendan and Alice’s creditors from acting against them for a period of 70-days, during which time their creditors are forced to deal with the PIP (if the creditors don’t engage with the PIP during the PC period, the PIA can proceed without the input of the creditor and could well see their entire debt written-off with no payments to that creditor). The table below is a summary of the debtors’ Prescribed Financial Statements (“PFS”).

THE PIA SOLUTION CONSTRUCTED BY THE PIP AND APPROVED BY CREDITORS

The PIP proposed interlocking PIAs for Brendan and Alice that restructured their mortgage loans on their family home and their investment properties in the following ways:

- The interest rate was reduced from 6.26% and fixed at 3.7% for the restructured term of their family home mortgage loan.

- The term was reduced to 276 months to from age 68 for Brendan.

- The mortgage balance owed was reduced by €138,378 to the current market value of the family home.

- The PIA provided for the sale of the two investment properties, with the residual shortfalls totalling €253,450 being treated as unsecured debt in the PIAs for Brendan and Alice.

- Monthly payments for 6 years are being made by Brendan and Alice (from income after their Reasonable Living Expenses have been provided for) to address creditors with unsecured debts that are to be written off at the end of the term of the PIA.

- Brendan and Alice retain their family home with a sustainable and performing mortgage loan.

Brendan and Alice are now solvent, and will continue to remain solvent so long as they adhere to the terms of their Personal Insolvency Arrangements. All their unsecured debts and €391,827 of mortgage will be written off in their PIAs.

The table hereunder shows the debts Brendan and Alice entered the Personal Insolvency process with, the payments made during the 6-years period of their PIAs, the amount of debt written off in the process, and the secured debt continuing after the process.

RATIONALE FOR CREDITORS’ SUPPORT OF PIAS FOR BRENDAN AND ALICE

The tables below detail the outcomes for Brendan and Alice’s creditors in a PIA scenario and in Bankruptcy. Creditors acted rationally, and in their own best interests, in supporting these PIAs. The table below details the differing outcomes for creditors between the PIAs and the alternative of bankruptcy.

CASE STUDY 4 -

BACKGROUND

John aged 46 lives in a modest 3 bed home in rural Co. Clare. He lives with his wife Mary and their two-primary school going children. John inherited the home he lives in as a dilapidated property and raised a mortgage from a sub-prime mortgage lender to update and modernize the house. John owned the property before he got married and took out the mortgage loan in his sole name.

John is a small sheep farmer with an off-farm job. Mary does not work outside the home. She looks after the couple’s two sons and takes case of the farm animals when John is at work.

John has only one debt other than his mortgage, a credit union loan. John fell into arrears on his mortgage when he had an accident on the farm and was unable to work for nearly a year. When he returned to work his income had dropped and both loan payments became unmanageable. John was deemed outside the Mortgage Arrears Resolution Process (MARP) without an alternative repayment arrangement being agreed with his mortgage lender.

It was at this point that John contacted his local MABS office. MABS advised he should meet with a Personal Insolvency Practitioner (“PIP”). John had seen the PIP Mitchell O’Brien interviewed on the RTE News, and following a search on the internet made contact by phone with Mitchell O’Brien in Waterford.

Within two weeks of having met with the PIP, the PIP had secured a Protective Certificate (“PC”), issued by the Western Circuit Personal Insolvency Court. The PC prevented both of John’s creditors from acting against him for a period of 70-days, during which time his creditors were forced to deal with the PIP (if the creditors don’t engage with the PIP during the PC period, the PIA can proceed without the input of the creditor and could well see their entire debt written-off with no payments to that creditor). The table below is a summary of the debtor’s Prescribed Financial Statement (“PFS”) at the start of the PIA process.

THE PIA SOLUTION CONSTRUCTED BY THE PIP AND APPROVED BY CREDITORS

The PIP proposed an individual PIA for John that restructured the mortgage on his family home in the following ways:

- The interest rate was reduced from 5.5% and fixed at 2.0% for the whole of the restructured mortgage term.

- The mortgage loan term was reduced to 249 months to age 68 John. Previously the mortgage loan term was to age 72.

- The mortgage balance owed was reduced to by €98,886 to the current market value of the property of €60,000.

- The monthly mortgage payment was reduced from €1,064 per month to €295 per month.

- The mortgage will continue to reduce each month during the PIA.

- John is making payments of €656 per month to his PIA in years 1 and 2, and €443 per month in years 3, 4, 5 and 6. These payments will be in full and final settlement of the unsecured credit union debt and the negative equity that was in his family home when John’s arrangement was approved by the relevant Court. The unsecured debt will receive a 24% dividend from this PIA.

- John and Mary retain their family home with a sustainable and performing mortgage loan.

John is now solvent, and will continue to remain solvent so long as he adheres to the terms of his Personal Insolvency Arrangement. His unsecured debts and €98,886 of his mortgage loan will be written off in his PIA.

The table hereunder shows the debts John entered the Personal Insolvency process with, the payments made during the 6-year period of the PIA, the amount of debt written off in the process, and the secured debt continuing after the process.

RATIONALE FOR CREDITORS’ SUPPORT OF PIAS FOR MR & MRS DEBTOR

The tables below detail the outcomes for John’s creditors in a PIA scenario and in Bankruptcy. Creditors acted rationally, and in their own best interests, in supporting this PIA. The table below details the differing outcomes for creditors between the PIA and the alternative of bankruptcy.

(C) O'Brien & Associates IP Waterford Limited T/A IRS IRELAND, 2021 - No. 4 Cois Mara, Galwey's Lane, Dungarvan, Co. Waterford, X35 K256

MITCHELL O'BRIEN IS AUTHORISED BY THE INSOLVENCY SERVICE OF IRELAND TO CARRY ON PRACTICE AS A PERSONAL INSOLVENCY PRACTITIONER, SINCE AUGUST 12TH, 2013 - ISI AUTHORISATION NO. PC00001

JESSICA O'BRIEN IS AUTHORISED BY THE INSOLVENCY SERVICE OF IRELAND TO CARRY ON PRACTICE AS A PERSONAL INSOLVENCY PRACTITIONER, SINCE DECEMBER 5TH, 2017 - ISI AUTHORISATION NO. PF00301

DENISE O'BRIEN IS AUTHORISED BY THE INSOLVENCY SERVICE OF IRELAND AS AN APPROVED INTERMEDIARY, SINCE OCTOBER 31ST, 2017 - ISI AUTHORISATION NO. AG00299